Save When You Can!

Just like how regular exercise is necessary for good health, so are good financial habits for a secure future. While some of us are good at saving any extra left over from our income after our expenses, some find ways to spend that away. Here we explore why it is critical to save.

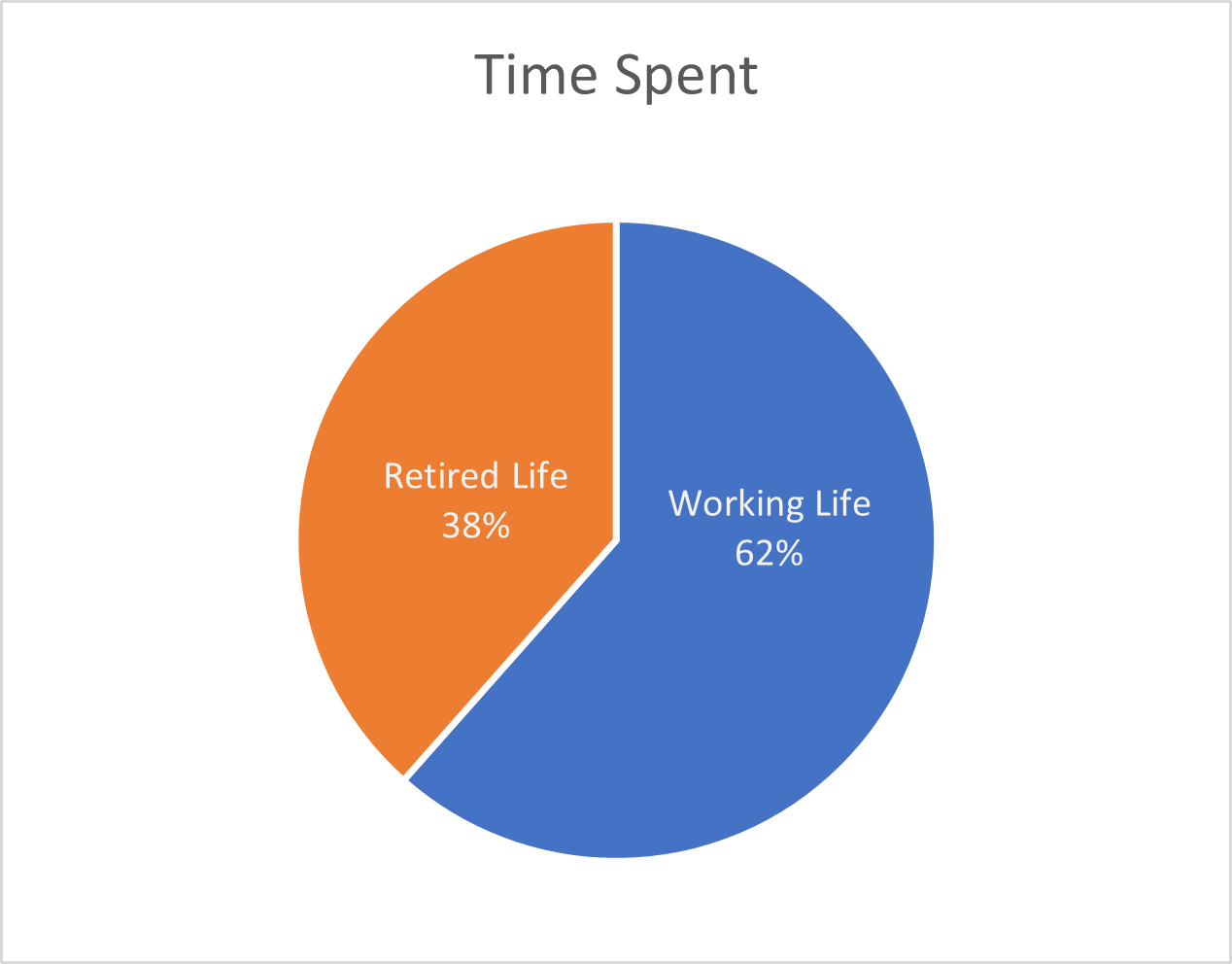

Consider someone starting their adult working life at age 25. They typically would work till age 65 and would have a life expectancy of age 90. This means they work for about 40 years and then have a retired life of 25 years, about half their working adult life

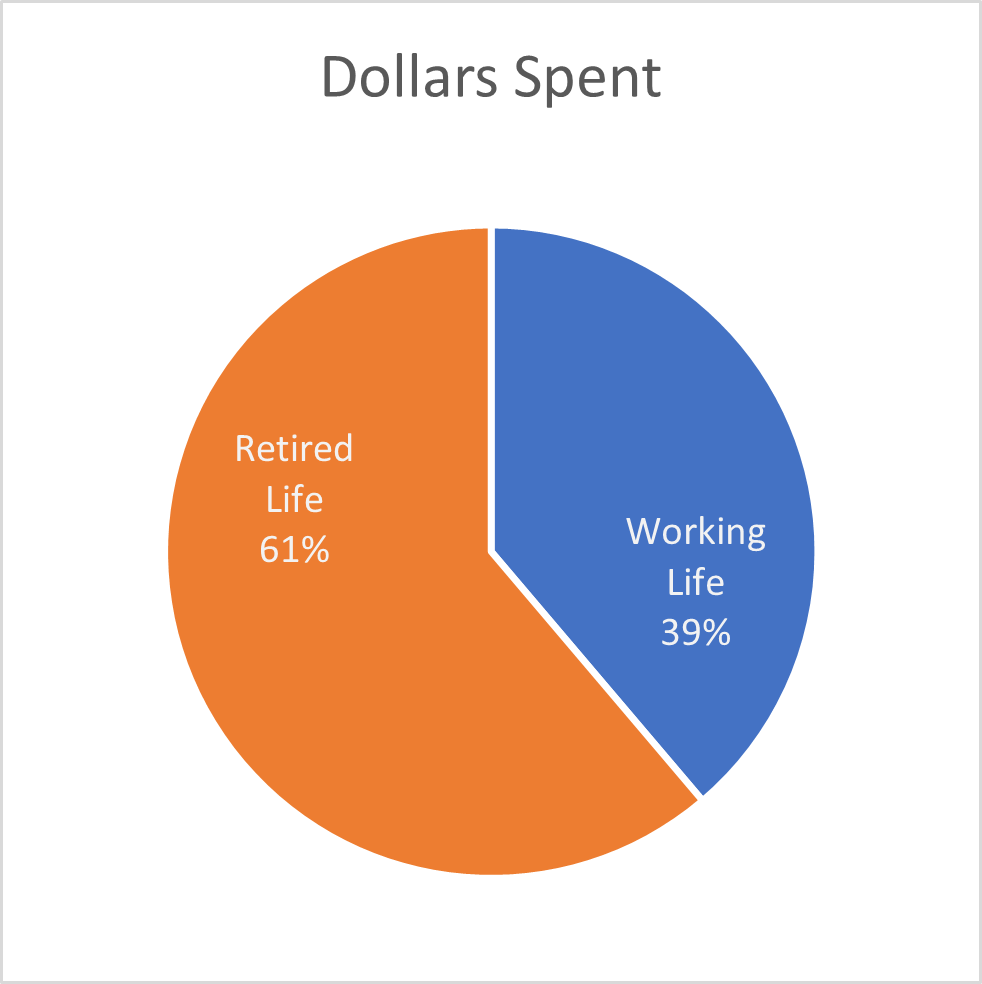

If their expenses grow with inflation at the rate of about 3% every year, the nominal dollars they spend in their retirement will be twice of what they will spend in their working life!! Typically, the expenses in retirement is lesser as folks scale down their lifestyle and may spend about 70% to 80% of what they would while they were working. If so, the proportion of nominal dollars spent in retirement is about the same as what is spent in working life.

It is interesting to look at how much one needs to save during their working life to afford their retirement.

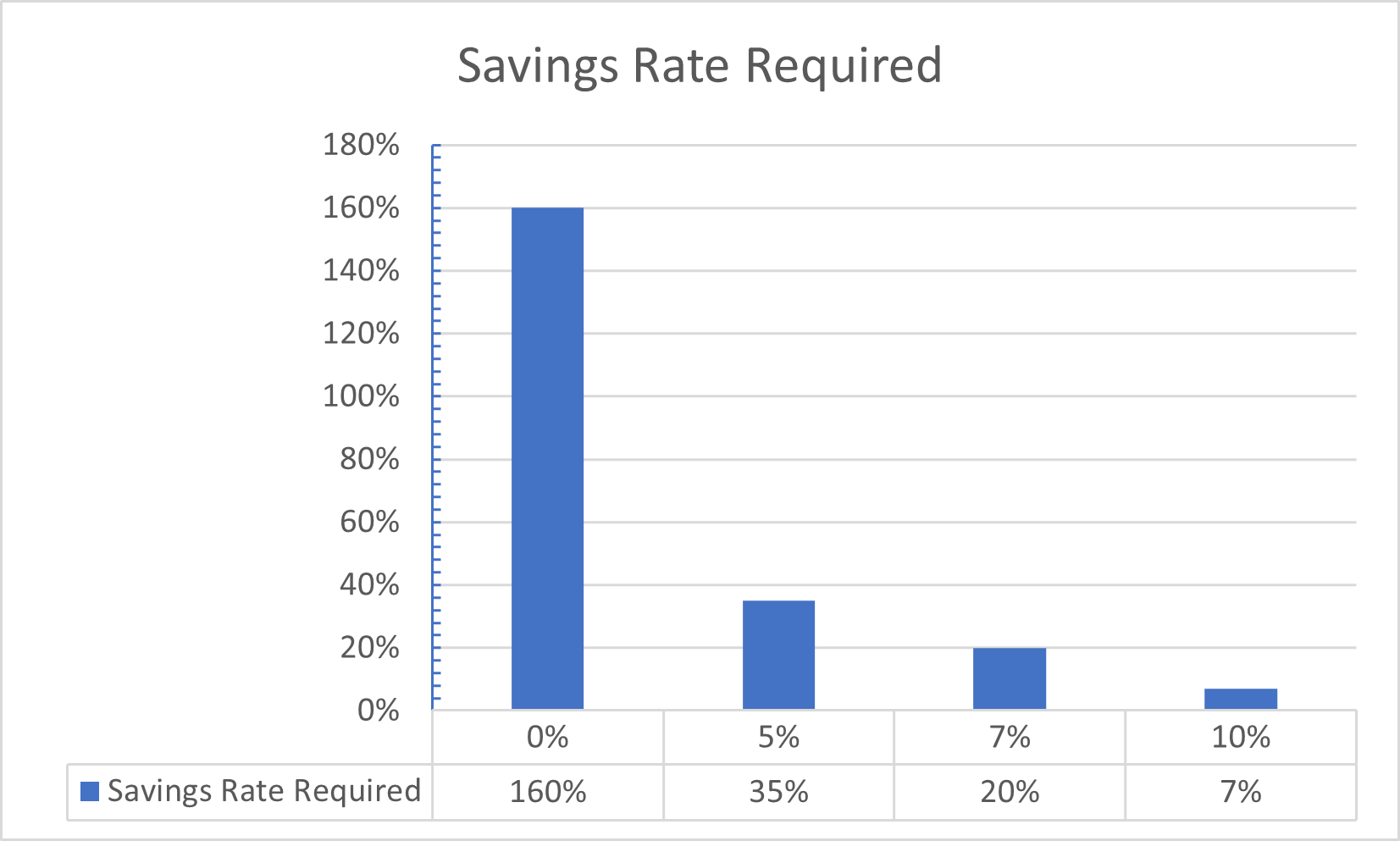

One key question that needs to be answered is how the savings will be invested during their working life. If they invest they savings conservatively, they will need to save a lot more. If they invest aggressively, they may need save a bit less. Whether you can save aggressively or not depends on various things including how far away you are from your retirement, what your risk tolerance is and so on. It is best to talk to your wealth advisor to get a better handle on this. We will simplify our assumptions here and assume there is a single savings vehicle we use for all our savings. While this is may not be realitic for your situation, it gives you a strong and simple mental model to remember.

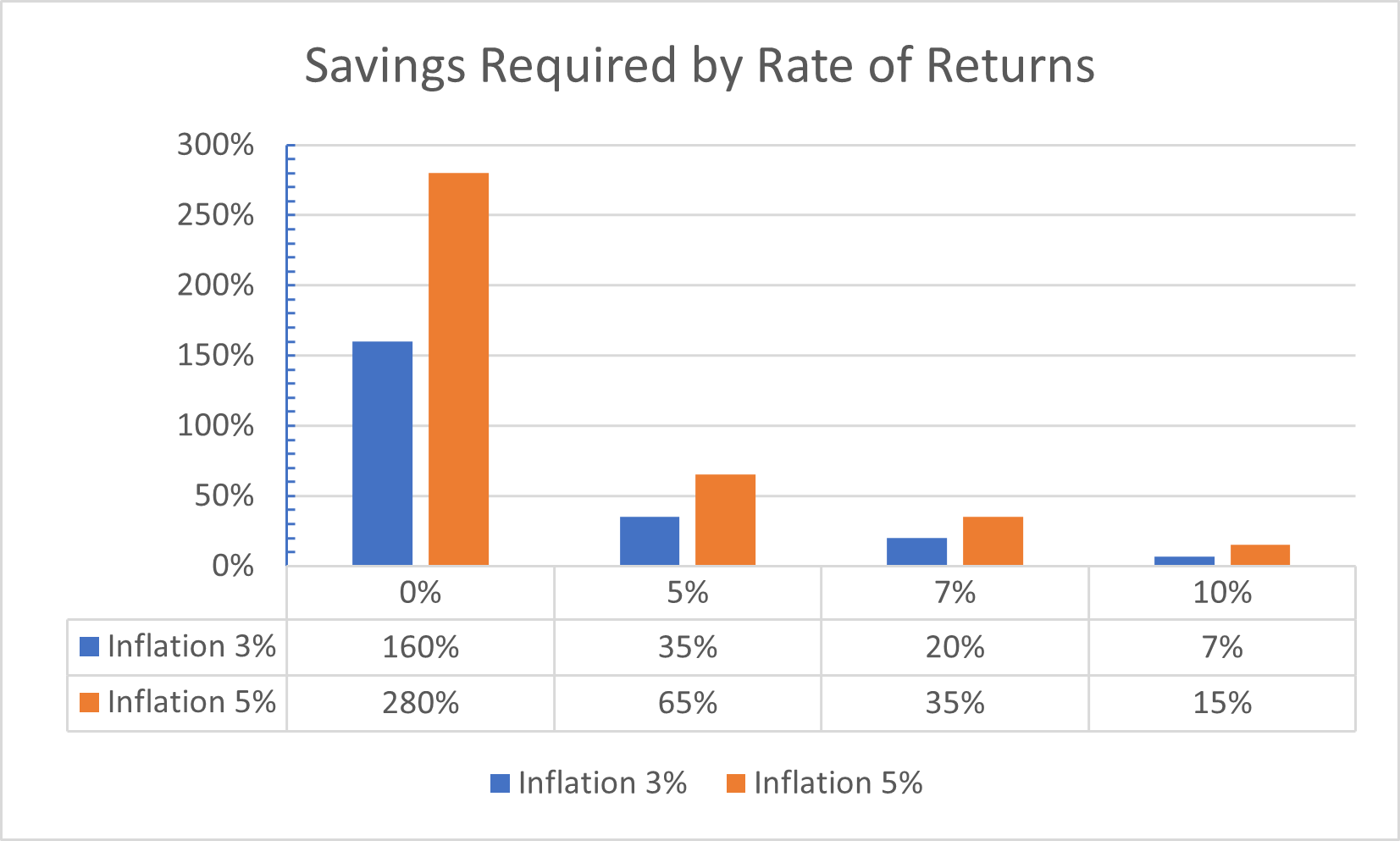

If you put all your savings in a bank, that earns almost no interest, you will need save 160% of your expenses every year. That is roughly $1.6 for every dollar you spend should be saved! If you save in bonds, real estate such as your home or other investments that produce around 5% of compounded interest, you will need to save about $1 for every 3 dollars you spend. If you are okay saving in higher risk investments such as the stock market, which on an average generates about 7% yearly compounded returns, you will need to save $1 for every 5 dollars you spend.

Of course, the money you save will also depend on inflation rate. If the inflation rate is around 3% as it is now, the above numbers will apply. If the inflation rate kicks higher, which it is likely to do in the future, the amount of savings would also need to go higher. For example, if the inflation rate picks up and stays at 5%, you will need to almost double your savings rate.

Next, let us look at the incentives IRS or Internal Revenue Service provides us to save. Every year, an individual can set aside their savings in a qualified retirement account such as a 401k plan or an IRA or individual retirement account. IRS allows you to take tax deferrals on the money saved during your working years. The money can also grow tax free until retirement. For a person starting out their working life, if their salary is $100,000 a round number for ease of recollection, IRS will allow them to save $19,500. They can also save an additional $6000 in IRA every year.

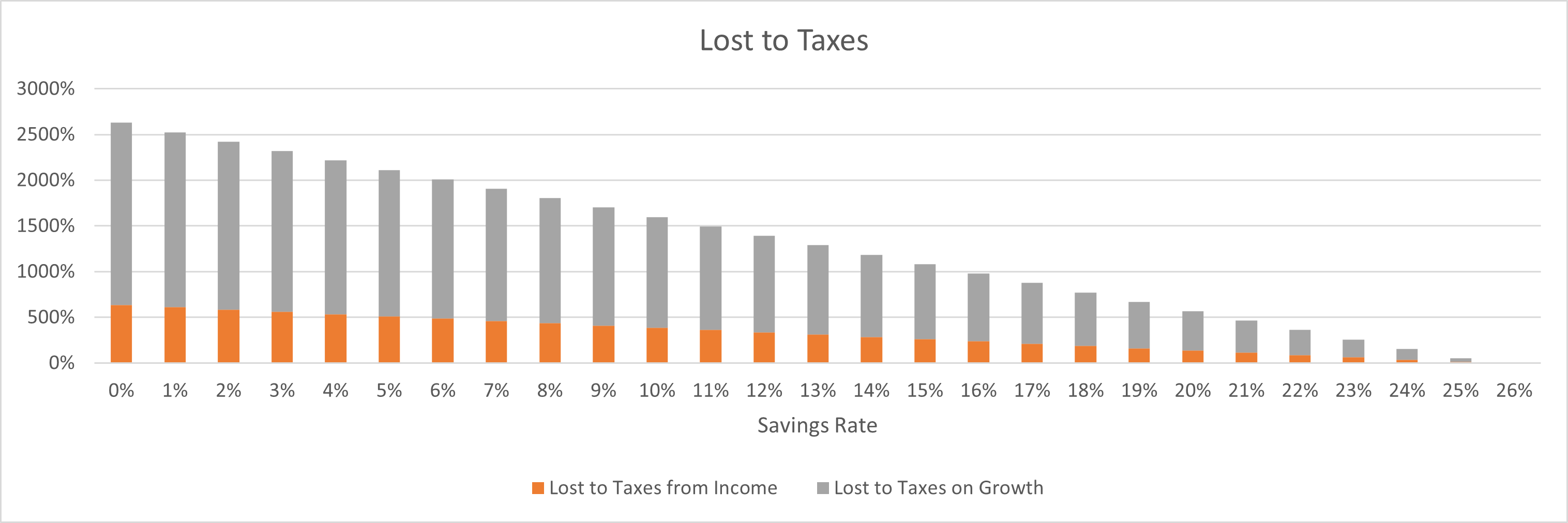

Most of the time, it is best to take full advantage of the incentives IRS offers you. If you do not save, you lose money because you are not taking advantage of this incentive. Here is an assessment of how much you are possibly losing if you do not fully utilize this benefit. Let us say the average tax rate, including state tax, through your working life is 33% and it drops down to 17% in retirement. If you save nothing in the retirements accounts with IRS incentives, you will pay IRS taxes for the money you are not saving in retirement accounts. This amount that you will pay as taxes is a whopping 25 times the above mentioned salary in nominal dollars throughout your lifetime. If you save only 10% of your salary, it will reduce this tax burden to 15 times the salary. You will need to save to the limits of contribution that IRS allows so you can save fully on these taxes.

Carrots or Sticks?

Some of us are motivated by carrots, while some of us are by the sticks. The incentives that IRS provides is a carrot if you think you are saving on taxes when you save in retirement accounts. If you think you are losing your money to taxes when you do not save in retirement accounts, it is a stick! Whichever way you like to get motivated, it is best to save your dollars when you are earning and when you CAN save!

#SaveWhenYouCan!!